Market Opportunity

We operate in a large, growing and highly fragmented market, with important defensive characteristics. We are strongly positioned for growth, with a significant market share opportunity.

The building

materials market1

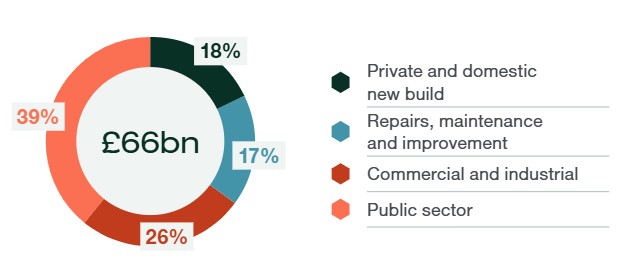

The UK building materials market totals £78 billion. Around £66 billion1 of this is serviced by distributors and therefore represents our addressable market. The repairs, maintenance and improvement (RMI) market is approximately 17% of the market and generated 79% of our revenues in 2025

The repairs, maintenance

and improvement market

Housing transactions, employment levels and interest rates are short-term lead indicators for RMI spend. Longer term, the outlook for RMI remains favourable as a result of:

- The age of the UK’s housing stock, which is among the oldest in Europe. Around 78% was built before 1980 and 38% before 19462. Older homes are much likelier to be in a poor state of repair and need regular maintenance

- Older homes also have lower energy efficiency, requiring improvements such as insulation, double glazing and low‑carbon heating to reduce energy costs and carbon emissions

- Home ownership is shifting from landlords to owner-occupiers, who have more incentive to invest in their properties. In 2024, landlords sold 5.4 houses to owner-occupiers for every one house they bought from owner-occupiers3, reflecting increased regulation, taxation and the high cost of finance driving landlords to reduce their holdings

Our other building

materials markets

| Target of new homes built by 2029 |

UK public sector property ownership |

| 1.5 million |

300,000 properties |

Other long-term drivers of demand for building materials include the need for more homes to meet the UK’s significant housing shortage. The Government continues to target 1.5 million new homes by 2029 and announced a series of measures in December 2025, including a consultation on the National Planning Policy Framework, to accelerate delivery. Our A.W. Lumb, Hevey and MAP brands all have exposure to new-build housing demand.

We also have exposure to the infrastructure sector through our George Lines brand. The Government recognises that investment in infrastructure is critical to achieving all its social and economic goals and it published a 10-year investment plan in June 2025, backed by at least £725 billion of Government funding over the next decade. The recently established National Infrastructure and Service Transformation Authority published the initial pipeline of projects in July 2025. As at January 2026, this included around £530 billion of identified projects with £285 billion of Government funding or 40% of the planned total.

More broadly, the UK public sector owns more than 300,000 individual properties. We see the need to invest in the substantial number of ageing public buildings as a potential market for us. Many of the UK’s commercial buildings also need investment, for example to meet more stringent energy efficiency standards, opening up further possibilities.

The UK

merchanting market

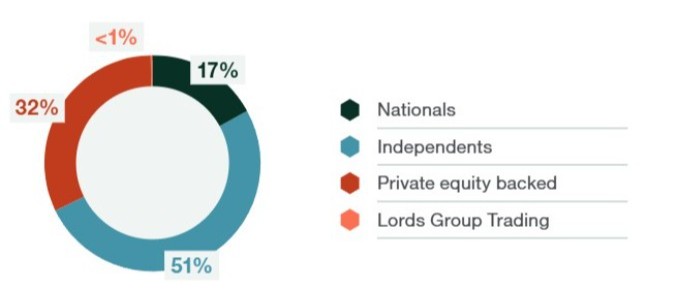

Our market is highly fragmented, with over 2,000 merchants listed in the national directory. The national chains make up 17% of the market by turnover, with 51% attributable to independent merchants, which are often family run. We currently account for less than 1% of the market.

The national chains have found it difficult to increase their market share and some have divested business units. Few independent merchants are pursuing a buy-and-build strategy like ours, and we therefore believe that we are very well placed to take further market share through consolidation, offering vendors a unique colleague and customer-first approach.

The plumbing and

heating market

P&H supplies independent plumbers’ merchants, alongside one other national competitor. We also sell directly to installers and homeowners, which is a more competitive market. Our digital presence and deep stock cover give us an advantage over some national competitors, who sell through more traditional channels.

Boilers currently generate around 66% of P&H’s revenues. Their natural replacement cycle means there is regular demand for them, and our P&H division typically has a market share of 10% to 11%. We rely on a small number of boiler suppliers, but we are a key route to market for them, and we are reducing our reliance over time by expanding our product range and signing exclusive distribution agreements with other manufacturers. Lower-carbon technology offers growth potential for us, and we are well placed to benefit from legislative changes regarding carbon efficiency of the UK’s housing stock.

1. Source: Travis Perkins plc investor website and 2025 Annual Report.

2. Source: HBF.

3. Source: Savills.